The thought of various government support measures expiring in the months ahead, causing some sort of fiscal cliff over which economies and share markets will plunge, has caused much consternation. But as with the original fiscal cliff of December 31, 2012 in the US, it’s likely to be tapered into a fiscal slope. Particularly with so called “second waves” of coronavirus reaping havoc with the economic outlook. Of course, this will add to the public sector’s debt burden associated with the coronavirus shock, in turn adding to concern about some sort of fiscal day of reckoning down the track.

This note looks at the key issues around fiscal support and the budget in Australia ahead of the Treasurer’s Economic Statement (due 23rd July) which is expected to provide new economic forecasts, an estimate of the budget cost of support measures so far and outline plans for future support measures.

Fiscal stimulus to be extended

It made sense for many of the coronavirus government support measures to expire at the end of September as it avoided a permanent/hard to reverse lift in public spending, and to borrow from the analogy likening the support measures to a bridge across a chasm, once the coronavirus chasm has been crossed there is no longer the need for the bridge. However, its increasingly clear that support will be needed for longer:

-

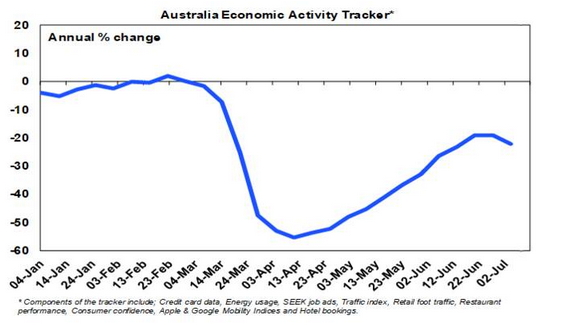

First, the second wave of coronavirus cases in Australia has seen the Victorian Government return Melbourne to a “stay at home” six-week lockdown which will slow the recovery. While we estimate the direct impact on the Australian economy to be around $5bn which will knock around 1% off GDP this quarter, there is a high risk that it impacts confidence in other states (as people “self-isolate”) and that other states may also return to a lockdown if cases spread, with NSW most at risk. This already appears to be impacting economic activity, with our Australian Economic Activity Tracker which combines timely weekly data faltering over the last two weeks, after ten consecutive weeks of recovery.

Source: AMP Capital

-

Second, the easy gains from the initial reopening including the unleashing of pent up demand may have mostly been seen but distancing requirements and travel restrictions mean that it will take much longer for some industries – travel, events, culture, accommodation, restaurants and housing construction – to get back to normal.

-

Third, the coronavirus shock has accelerated the shift to a digital world, such that job losses associated with automation are now likely occurring faster than new jobs are being created. Three examples of this are a faster take up of online retailing meaning less jobs in retailing, more working from home meaning less office demand and less jobs in public transport and less business travel in favour of virtual meetings meaning less use of airlines and hotels.

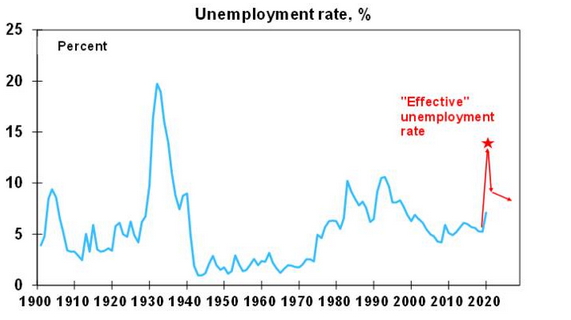

The last two mean that “spare capacity” will linger well into the future and this is likely to show up in a long tail of high unemployment. Without the JobKeeper wage subsidy and changes to JobSeeker, “effective unemployment” would have risen to 14.8% in April and would still be around 13.6% now.

Source: RBA, ABS, AMP Capital

The initial spike in “effective unemployment” may be reversed quickly taking it down to say 9% by year end, but getting it back to 5% as seen early this year could take years as some sectors take a long time to recover and accelerated structural change impacts. This suggests both a short-term and a long-term challenge for government which will likely be met at least in the short term by more fiscal stimulus.

Revised budget deficit projections

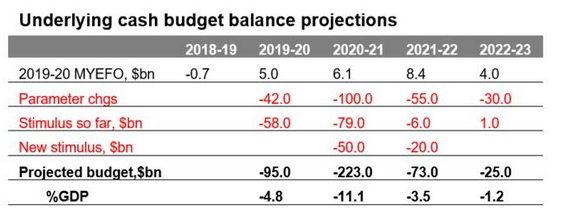

Our revised deficit projections are shown below and take the December 2019 Mid-Year Fiscal Outlook as the starting point.

Source: Australian Treasury, AMP Capital

The hit to the economy will mean a hit to government revenue and this is shown in the line called “parameter changes”. Budget data released for the period to May suggests that this has been running at just over $10bn a month since March.

The Government has already announced significant policy support and this is shown in the line “stimulus so far”. We have allowed for the three policy support packages in March, the health package and industry support packages. These are dominated by JobKeeper now estimated to cost $70bn.

However, the need for additional support for the economy has also been recognised by the

Government. As a result, in its 23 July economic statement we are likely to see:

-

An extension of JobKeeper – although it’s likely to be revamped with a monthly eligibility test and different pay rates and companies are likely to be discouraged from accessing it for jobs that won’t be revived;

-

The doubled JobSeeker payment is likely to be pared back;

-

Income tax cuts due from 2022 may be brought forward;

-

Additional investment incentives; and

-

More industry support packages.

The Government will partly fund extra support by taking JobKeeper from those who no longer need it, but the bulk will likely come from the $60bn saving already seen on JobKeeper, which we expect to be fully spent and then some (see “new stimulus”) although it may not all be announce next week.

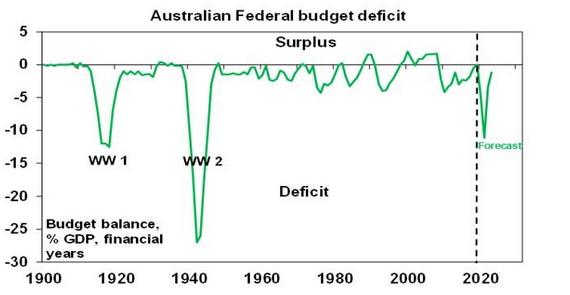

As a result of the Government’s fiscal response and the hit to public revenue from the economic downturn, the budget deficit is expected to blow out from around $95bn for the past financial year to around $223bn this financial year before improving from 2021-22, as support programs phase down and the economy recovers. This would see the budget deficit as a share of GDP peak at around 11% of GDP in 2020-21, which would be its highest since World War 2. Spread over several years, this will add nearly 20% of GDP to Australia’s public debt. This raises two questions though: will it be enough? And can we afford it?

Source: RBA, Australian Treasury, AMP Capital

Will it be enough?

By extending programs like JobKeeper beyond September and announcing additional stimulus including the likely bring forward of tax cuts, the Government will effectively taper the fiscal cliff and turn it into more of a slope. This helps solve the short-term reality that a lot of jobs won’t have come back by October. However, it remains to be seen whether this will be enough given the long tail of unemployment flowing from the coronavirus shock discussed earlier. The Government’s focus looks likely to shift to economic reforms in the October budget and this makes sense, but more fiscal support may ultimately be needed to soak up the likely long tail of unemployment.

Can we afford the surge in the deficit and debt?

Our assessment remains that it is affordable. First, were it not for the support measures the economic hit would be far greater, ultimately resulting in an even bigger public debt blowout.

Second, as Keynes showed, it makes sense for the public sector to borrow from households and businesses at a time when they have cut their spending, and to give the borrowed funds to help those businesses and individuals that need help.

Third, the support programs won’t cause a permanent step jump higher in public spending.

Fourth, Australia’s starting point for net public debt was low at 23% of GDP compared with other advanced countries averaging 83%. See the next chart. And even with projected budget deficits it will remain relatively small.

Source: IMF, AMP Capital

Fifth, borrowing to finance the budget deficit is in Australian dollars and, with a current account balance, we are not dependent on foreign creditors risking a foreign currency crisis.

Sixth, the cost of Government borrowing is very low at less than 1% for ten years. This is partly being facilitated by the RBA buying bonds, but bond rates would be low anyway.

Finally, consider what would happen if “shock horror” the Government and the RBA agreed to cancel the bonds that the RBA owns? Apart from a lot of grinding teeth from some commentators the answer would be very little – the Government’s loss on its “investment” in the RBA would be offset by a reduction in liabilities. In other words, it’s not necessarily the case that all public debt has to be paid back if it’s owned by the central bank. For the technically minded, the limit to this would be if all the extra money that the central bank printed to buy the bonds causes inflation – but as Japan has seen, if there is lots of spare capacity, inflation is not an issue.

Concluding comment

With the private sector spending hit by coronavirus it makes sense for the Government to continue to help fill the breach and support the economy. The best approach to getting debt back down is to grow the economy aided by a reinvigorated economic reform agenda, but for a while government fiscal support will continue to be needed.

Source: AMP Capital 15 July 2020

Important notes: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) (AMP Capital) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided and must not be provided to any other person or entity without the express written consent of AMP Capital.